7 Fatal Mistakes Homeowners Make During Insurance Claims

7 Fatal Mistakes Homeowners Make During Insurance Claims

7 Fatal Mistakes Homeowners Make During Insurance Claims

When disaster strikes your home: whether it’s a burst pipe, a hurricane, or a kitchen fire: your first instinct is likely relief that you have insurance. You’ve paid your premiums on time for years, and now it’s time for the "good neighbor" to step in.

Here is the cold, hard reality: Insurance is a contract, not a social safety net.

The moment you file a claim, you enter a high-stakes business negotiation with a multi-billion dollar corporation. Their goal is to minimize their liability; your goal is to restore your home. Unfortunately, the playing field is not level. Most homeowners unknowingly commit "fatal mistakes" during the claims process that lead to denied, delayed, or significantly underpaid insurance claims.

At Adkinson Insurance Services, we see these errors every day. If you want to protect your largest asset, you must avoid these seven common pitfalls.

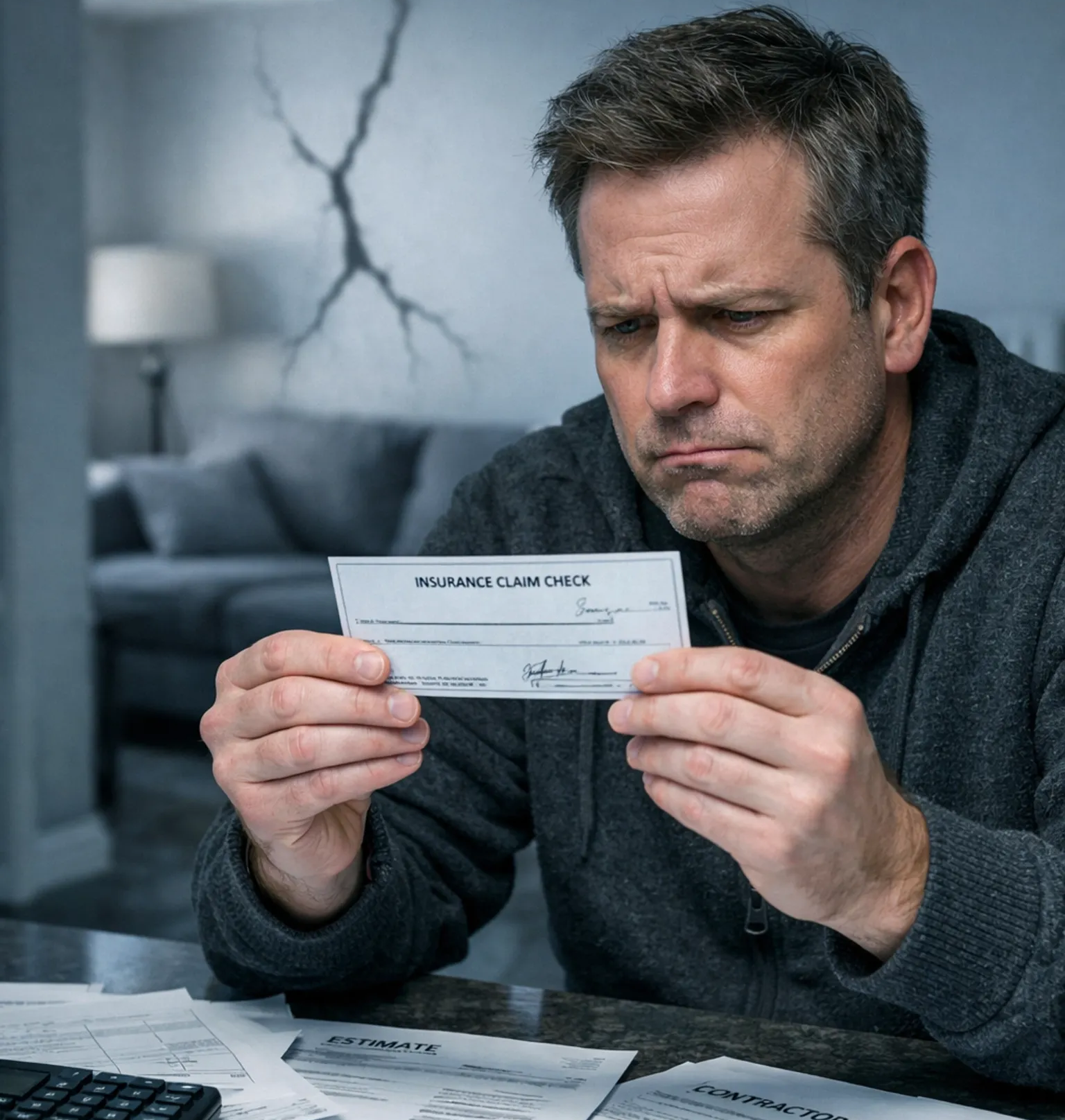

1. Accepting the First Offer Without Negotiation

This is the most frequent mistake we encounter. When a check arrives in the mail from your insurance carrier, it often feels like a win. However, that initial offer is rarely the full value of your loss.

In the industry, we often see carriers provide an "undisputed amount." This is the bare minimum they admit they owe you. They might use a software called Xactimate to calculate costs, but they often use "builder’s grade" pricing or omit necessary line items like local permit fees, debris removal, or the actual cost of high-end materials.

- The Trap: Homeowners sign a release or assume the first check is the final word.

- The Reality: That check should be viewed as a down payment. You have the right to demand a "supplemental" payment for the items they missed or undervalued.

2. Not Documenting the Damage Properly

The burden of proof in an insurance claim lies entirely on you, the policyholder. If you cannot prove the damage existed: or that it was caused by a covered peril: the insurance company has no obligation to pay.

Many homeowners take three or four blurry photos and think that is enough. It isn’t. You need a comprehensive digital inventory of the loss.

- Photos and Videos: Capture the damage from multiple angles. Take wide shots to show the scope of the room and close-ups to show the detail of the damage (like ceiling stains or roof damages).

- Inventory Lists: Don't just say "electronics." List the make, model, and serial number.

- The "Before" Factor: If you have photos of your home before the damage, they are worth their weight in gold. They prove the damage is "new" and not "pre-existing wear and tear": a favorite excuse for claim denials.

3. Waiting Too Long to File or Report Damage

In Florida, timing is everything. Whether you are dealing with hail or a tornado, your policy likely contains a clause requiring "prompt notice" of the loss.

Waiting weeks or months to report a claim gives the insurance company a massive advantage. They can argue that the damage worsened because you didn't report it, or that a secondary issue (like mold) occurred because of your negligence.

- Statutory Deadlines: Florida law and individual policy language have strict "Statutes of Limitations." If you miss these windows, your claim is dead on arrival.

- Evidence Decays: Walls get painted, roofs get patched, and water dries up. The longer you wait, the harder it is for a public adjuster in Florida to reconstruct the scene and fight for your settlement.

4. Not Understanding How Depreciation Affects the Settlement

Most homeowners don't realize there are two ways a claim can be paid: Actual Cash Value (ACV) or Replacement Cost Value (RCV).

- ACV: This is the "yard sale" value. The carrier takes the cost of the item and subtracts "depreciation" based on its age.

- RCV: This is the cost to actually buy a new version of that item today.

The mistake happens when homeowners see a massive "depreciation" deduction on their settlement summary and assume that money is gone forever. In many RCV policies, that depreciation is "recoverable." You can get that money back once the work is actually completed. However, if you don't understand how to trigger that payment, the insurance company keeps your money.

5. Trusting the Insurance Company’s Adjuster Blindly

When your carrier sends an adjuster to your house, they may be friendly, professional, and empathetic. But you must remember: They work for the insurance company.

Their paycheck, their training, and their performance reviews are all handled by the entity that owes you money. Their job is to find reasons to limit the payout. They might overlook a "scope gap": such as failing to notice that water has seeped behind the baseboards or into the subfloor: which could lead to a comprehensive mold inspection being necessary later.

Never assume the carrier's adjuster has found everything. They are often incentivized to spend as little time as possible on your property.

6. Not Keeping Receipts for Emergency Repairs

Your insurance policy is a two-way street. You have a "duty to mitigate" further damage. This means if you have a hole in your roof, you must tarp it. If you have a broken pipe, you must shut off the water and call a restoration company to dry out the area.

However, many homeowners pay for these emergency services out of pocket and lose the receipts, or they don't realize these costs are reimbursable in addition to the property damage settlement.

- Keep Everything: Every roll of duct tape, every tarp, and every hour of professional labor should be documented.

- Emergency vs. Permanent: Do not make permanent repairs (like replacing the whole roof) until the adjuster has seen it. Stick to temporary fixes that prevent the "loss" from getting worse.

7. Attempting to Navigate the Process Without Professional Help

The biggest mistake of all is believing that you can handle a complex property insurance claim alone against a team of corporate lawyers and adjusters. The insurance policy is a dense legal document, often hundreds of pages long, filled with exclusions, endorsements, and conditions.

Attempting to DIY your claim is like going to court without an attorney. You are at a severe disadvantage.

This is where a public adjuster in Florida comes in. Unlike the carrier’s adjuster, a public adjuster works exclusively for you.

Why a Public Adjuster is the Solution

At Adkinson Insurance Services, we serve as your protective ally. Our job is to level the playing field by bringing the same level of expertise to your side of the table that the insurance company has on theirs.

We Work on Contingency

One of the biggest hurdles for homeowners is the fear of more out-of-pocket costs. We operate on a contingency basis. This means:

- No upfront costs.

- No out-of-pocket fees.

- We don't get paid unless you do.

Our interests are perfectly aligned with yours. The more we recover for you, the more we earn. This "no-risk" model allows you to get property insurance claim help without adding to your financial stress.

We Uncover the "Hidden" Damage

We don't just look at the surface. We look for the "scope gaps" the carrier missed. Whether it’s fire, lightning, or hidden water damage, we use professional tools and industry knowledge to ensure every penny of your loss is accounted for.

We Handle the Bureaucracy

From filing the initial paperwork to negotiating with the carrier’s adjusters and filing supplemental demands, we take the burden off your shoulders. We understand the "language" of insurance and know how to counter their arguments with facts and data.

Don’t Settle for Less Than You Deserve

If you feel like your claim is being stalled, or if you are looking at a settlement that won't even cover half of your contractor's estimate, you need underpaid insurance claim help.

Insurance companies count on homeowners being too tired or too confused to fight back. Don't let them win by default. Your home is your sanctuary: ensure you have the funds to restore it properly.

Ready for clarity on your claim?

Review our

Resources or see

how it works. If you're tired of the runaround,

contact us today for a free, no-obligation claim review. Let’s get your home back to the way it was.